Advising on Cayman Islands Trusts or British Virgin Islands (BVI) Trusts

06 August 2024 . 8 min read1. Overview

The laws relating to trusts and equity in the Cayman Islands and in the British Virgin Islands are derived directly from English law but have been modified in each jurisdiction by legislation to reflect their respective position as a premier offshore financial centre.

A trust is a legally binding arrangement whereby a person (“Settlor”) transfers assets to another person (“Trustee”) who is entrusted by the Settlor with legal title to the trust assets, not for the Trustee’s own benefit, but for the benefit of other persons (known as “Beneficiaries”, who may include the Settlor) or for a specified purpose. In addition to being a Beneficiary, the Settlor may, in certain circumstances, also act as a co-Trustee. The Settlor may, also, retain a degree of control over the trust, such as the power to approve distributions, the power to appoint and remove Trustees and the power to revoke the trust.

The Settlor will set out detailed instructions to the Trustee as to the disposition of trust assets in a document called the Declaration of Trust or the Trust Deed. This document will inform the Settlor, the Trustee and the Beneficiaries as to their respective rights, entitlements and duties.

2. Setting up a Trust – Who will be the Trustee?

The Trustees or Trustee of a Cayman Islands Trust or a BVI Trust (i) may be individuals, or (ii) may be a company licenced as a trust company in the Cayman Islands for Cayman Trusts or in the BVI for BVI Trusts (except in each case, for a Private Trust Company (“PTC”) which does not have to be licensed). An individual Trustee does not have to be a Cayman resident or a BVI resident to be a trustee of a Cayman Trust or a BVI Trust.

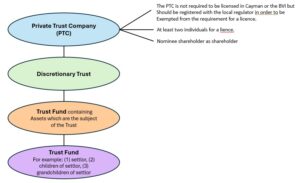

Corporate Trustees

Generally, the Trustee of a Cayman Trust is a trust company based in Cayman or the Trustee of a BVI Trust is a trust company based in the BVI. This can be either (i) a licensed Trust Company which carry on business as a professional trustee, or (ii) a PTC.

Generally, a PTC acts as Trustee of a single trust or a group of related trusts and does not charge fees. For example, instead of using the services of a professional Corporate Trustee in Cayman or in the BVI, the Settlor could establish a PTC in Cayman or in the BVI (as applicable) to act as Trustee of the trust mentioned below. The Settlor or his trusted advisors can serve on the board of directors of the PTC, which allows the Settlor more flexibility, control and continuity in the administration of the trust’s assets. PTCs can also be a more cost-effective solution in certain instances. A PTC in either Cayman or in the BVI is exempt from the regulation and licensing requirements in Cayman or in the BVI (as applicable), subject to certain requirements.

3. Type of Offshore Trusts

There are various types of trusts in each of the Cayman Islands and the BVI. The most appropriate trust structure for the settlement of trust assets will depend on the Settlor’s particular circumstances and the Settlor’s objectives. The most common types of offshore Trusts are (1) Discretionary Trusts, (2) Fixed Interest Trusts, (3) Accumulation and Maintenance Trusts, (4) Revocable Trusts, (5) VISTA trusts for the BVI, (6) STAR Trusts for the Cayman Islands, and (7) Non-Charitable Purpose Trusts.

Discretionary Trust

The discretionary trust provides a flexible and efficient structure under which the Settlor transfers ownership of the assets to the Trustee(s), subject to any reserved powers or Protector provisions. The settlement deed generally gives the Trustee(s) wide discretionary powers over the trust fund and its application for the benefit of the Beneficiaries. The Beneficiaries of a discretionary trust have no definite right to the assets of the trust.

Fixed Interest Trust

A fixed interest trust specifies the rights of Beneficiaries in relation to the capital and/or income of the trust fund. For example, the settlement deed may specify that a Beneficiary is entitled to the income (and not the capital) of the trust fund during his/her lifetime. A trust can also be structured as a combination of a discretionary and a fixed interest trust.

Accumulation and Maintenance Trust

An Accumulation and Maintenance Trust (“A&M Trust”) is a type of discretionary trust where one or more Beneficiaries will become legally entitled to the income, or both capital and income, of the trust on attaining a specified age. A&M Trusts are generally used to benefit children or grandchildren of the Settlor. The Beneficiaries do not have a fixed entitlement to the benefits or interests accruing to the trust for a certain period, during which time income is accumulated and as it grows is added to the capital assets of the trust. The persons who are ultimately entitled to the trust assets may benefit from the accumulation of capital in the trust. The trust deed may give the Trustee a discretionary power to make distributions amongst the Beneficiaries up to a specific age for their education, maintenance and wellbeing and to provide thereafter for a designated share of the trust fund to be distributed to each child on attaining a specified age.

VISTA Trust

The VISTA trust is unique to the BVI. The main features of a VISTA trust are: (a) it may only hold shares of an underlying BVI company, although the company is not restricted in what it may invest in; (b) the Trustee is not under a duty to diversify or monitor the trust fund and investments, which is a basic principle of the more standard trusts; (c) at least one of the Trustees must be a ‘designated Trustee’ as defined in the VISTA Act (for example a PTC or a BVI licensed trust company); and (d) the Trustee cannot act as a director of the underlying company.

STAR Trust

The STAR Trust is unique to the Cayman Islands. The Special Trusts (Alternative Regime) Act, 1997 is now incorporated into Part VIII of the Trusts Act (As Revised) (“Trust Act”. The key features of the STAR Trust are that:

- Beneficiaries and/or objects may be persons, purposes or both. There may be any number of Beneficiaries and any number of purposes, whether charitable or not, provided that such purposes/objects are lawful and not contrary to public policy in Cayman.

- Any uncertainty as to the objects or mode of execution or administration of a STAR trust can be resolved by the Trustee (or any other person the STAR trust document so specifies) or by the Cayman court, if necessary. A STAR trust is therefore very unlikely to be declared void from the outset on grounds of uncertainty, as could be the case with a poorly drafted non-STAR trusts.

- The Trustee of a STAR trust must be or must include a trust company licensed to conduct trust business in the Cayman Islands. This adds a level of oversight and regulation above and beyond other jurisdictions. There are criminal sanctions attached if these requirements are overlooked or bypassed.

- STAR trusts must have an “Enforcer” who is the only individual person or corporate entity with legal standing to enforce the terms of the STAR trust (such enforcement powers having been removed from the Beneficiaries by virtue of the Trust Act). The Trust Act therefore makes a clear distinction between the capacity to benefit from a STAR trust and the actual capacity to enforce such a trust. The effect is to remove rights of Beneficiaries not only to enforce the trust, but also their right to seek disclosure of information regarding the STAR trust and its ongoing administration.

- The rule against perpetuities does not apply to STAR trusts, which may be created for an unlimited duration (or not, depending on the terms of the trust deed), which eliminates the risk of a resulting trust in favour of the Settlor at the end of the perpetuity period and the adverse tax consequences which may flow from such an event.

- A STAR trust cannot hold land in the Cayman Islands but may hold an interest in a company, partnership or other entity which does.

Non-Charitable Purpose Trust

A Cayman Trust or a BVI Trust can be established partly or wholly for non-charitable purposes. The purpose must be specific, reasonable and possible, and may not be immoral, contrary to public policy or unlawful. An enforcer must be appointed who shall have the duty to ensure the Trustee fulfils the non-charitable purposes of the trust. At least one Trustee must be a “designated person” (for example a PTC or a licensed trust company). A purpose trust may exist in perpetuity or be terminated at a specified date.

4. Key Advantages of Offshore trusts

Tax Planning: Offshore trusts are very popular because they are established in jurisdictions such as the Cayman Islands or the British Virgin Islands where the trustees are resident and are subject to zero tax and this brings with it a number of tax planning advantages, even though the tax position of the Settlor and/or the Beneficiaries has to be considered.

Confidentiality: Trustees of offshore trusts have a duty under common law to keep the affairs of the trust confidential. Whilst this duty is not absolute, the courts of the Cayman Islands and the BVI have an inherent supervisory jurisdiction over the administration of trusts and are generally unwilling to sanction the disclosure of information except in cases to avoid potential injustice or harm.

Asset Protection: Global operations may expose the Settlor’s business to different legal and financial challenges. Offshore trusts can protect the Settlor’s finances from lawsuits, bankruptcy actions and political instability in onshore jurisdictions and secure the business’s continuity in these circumstances.

Succession Planning: Changing leadership and ownership within a family business can bring unique complexities. Offshore trusts offer a clear and efficient framework for succession planning where distributions and management roles for future generations can be clearly set out and help prevent potential conflicts among family members and build transparency.

Flexibility and Control: Offshore trusts provide flexibility in that they can be customized to align with the Settlor’s specific goals (e.g. asset protection, philanthropy, or wealth distribution over multiple generations). The Settlor can also retain varying degrees of control over the trust, ensuring his/her vision remains in focus.

Freedom from Onshore rules and regulation: Establishing an offshore trust avoids specific rules relating to trusts onshore which may add additional regulatory and/or compliance burdens.

5. Common uses for Cayman Trusts and BVI Trusts

- As an instrument for succession planning in the event of death or incapacity.

- To mitigate against tax liabilities.

- To protect assets (e.g. from exchange controls or other government interference)

- As a confidential way of holding assets.

- To protect beneficiaries who have difficulty in managing their own affairs.

- To circumvent forced heirship rules.

- To hold shares in a family company or in corporate transactions.

- As a vehicle for philanthropic giving.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: ivy.wong@loebsmith.com

E. elizabeth.kenny@loebsmith.com

E: cesare.bandini@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

E: max.lee@loebsmith.com

E: frost.wu@loebsmith.com

E: edmond.fung@loebsmith.com